Looking for a personal loan with low interest to fund something important — like consolidating debt, covering emergency expenses, or financing a big purchase? The interest rate you pay can make a huge difference in your total cost over time. Here’s a clear guide to help you secure the best low-interest personal loan possible 👇

📉 What Is a Low-Interest Personal Loan?

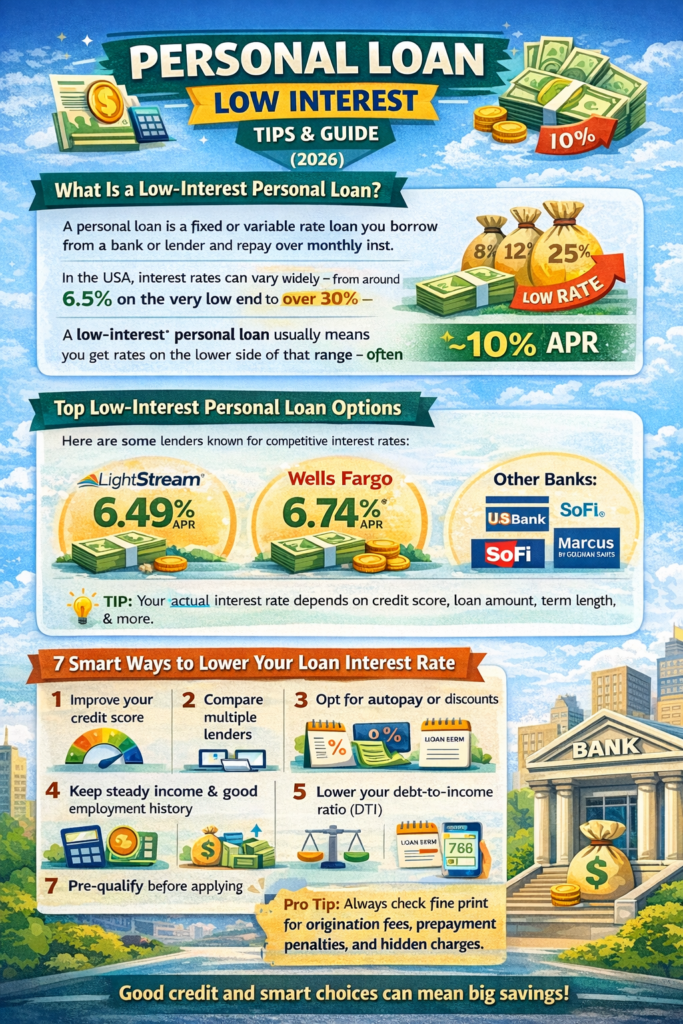

A personal loan is a fixed or variable rate loan you borrow from a bank or lender and repay over monthly installments. In the USA, interest rates can vary widely — from around 6.5% on the very low end to over 30% — depending on your credit, income, and loan terms. �

Forbes +1

A low-interest personal loan usually means you get rates on the lower side of that range — often under ~10% APR — especially if you have strong credit and stable finances. �

Forbes

💼 Top Examples of Low-Interest Personal Loan Options

Here are some lenders known for competitive interest rates (actual approval and APR depend on your credit profile):

LightStream — Loans with APR as low as ~6.49% with autopay setup. �

Forbes

Wells Fargo — Personal loans from about ~6.74% APR with discounts for certain customers. �

wellsfargo.com

U.S. Bank, SoFi, Marcus by Goldman Sachs — Other big lenders offering a range of low to moderate APR options depending on credit. �

Forbes

💡 Tip: Your actual interest rate will depend on credit score, loan amount, term length, and other factors. �

Forbes

🛠 7 Smart Ways to Lower Your Loan Interest Rate

Want the lowest possible monthly cost? Here are proven strategies:

- Improve your credit score

A higher credit score signals reliability to lenders and typically earns you lower interest rates. �

RupeeQ - Compare multiple lenders

Different banks and online lenders quote different APRs — shop around online to find the best deal. �

mint - Opt for autopay or discounts

Some lenders offer small rate discounts (e.g., 0.25–0.50%) if you enroll in automatic payments. �

Forbes - Keep steady income & good employment history

Stable income and financial history can boost your eligibility for better interest rates. �

Bankrate - Lower your debt-to-income ratio (DTI)

Lenders prefer borrowers with low existing debt compared to income — aim for a DTI under ~36–40% for best rates. �

Bankrate - Shorter loan term

Short terms usually come with lower interest cost — but higher monthly payments. �

IDFC First Bank - Pre-qualify before applying

Many lenders let you see estimated rates without a hard credit check, so you can compare offers without hurting your score. �

Bankrate

🧠 Final Takeaway

A low-interest personal loan can save you hundreds or even thousands in interest costs — especially when used wisely for debt consolidation or essential expenses. Key factors? Good credit, smart shopping among lenders, and strategic loan choices. �

mint

💰 Pro tip: Always read the fine print — look out for origination fees, prepayment penalties, and hidden charges that can affect your total cost. �