Life is full of uncertainties, but one thing remains constant: the need to protect the people who matter most. Life insurance in the UK is more than just a financial product—it’s a promise. A promise that your loved ones will be supported, no matter what happens.

Whether you’re starting a family, buying a home, or simply planning ahead, understanding life insurance can help you make confident, informed decisions about your future.

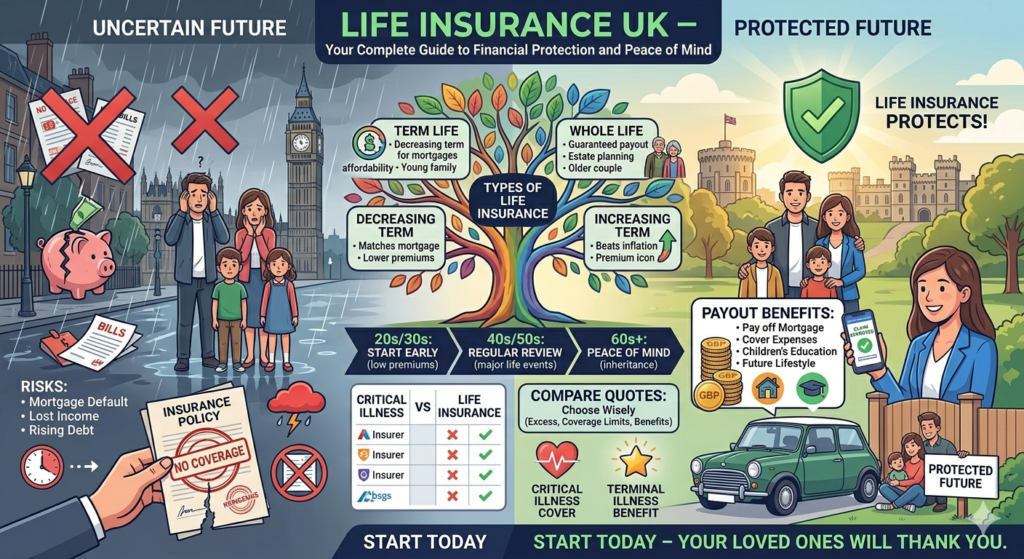

🌟 What Is Life Insurance?

Life insurance is a policy between you and an insurer. You pay regular premiums, and in return, the insurer pays out a lump sum if you pass away during the policy term.

This payout can help your family:

- Cover daily living expenses

- Pay off debts like mortgages

- Fund children’s education

- Maintain their standard of living

It’s not about expecting the worst—it’s about preparing for it wisely.

🇬🇧 Why Life Insurance Matters in the UK

In the UK, many households rely on a single or dual income to manage expenses. Without financial protection, the loss of an income can be devastating.

Life insurance ensures:

- Financial stability for your dependents

- Protection against rising living costs

- Peace of mind knowing your family is secure

With inflation and economic changes, having a safety net is more important than ever.

🛡️ Types of Life Insurance in the UK

Understanding different types of life insurance helps you choose the right policy for your needs.

1. Term Life Insurance

This is the most common and affordable option.

✔️ Key Features:

- Covers you for a fixed period (e.g., 10, 20, or 30 years)

- Pays out only if you pass away during the term

- Lower premiums compared to other types

👉 Ideal for:

- Mortgage protection

- Young families

- Budget-conscious individuals

2. Whole Life Insurance

This policy covers you for your entire lifetime.

✔️ Key Features:

- Guaranteed payout whenever you pass away

- Higher premiums

- Can include investment components

👉 Ideal for:

- Estate planning

- Leaving an inheritance

- Long-term financial security

3. Decreasing Term Insurance

Often used for mortgages.

✔️ Key Features:

- Coverage decreases over time

- Lower premiums

- Matches reducing loan balances

👉 Ideal for:

- Repayment mortgages

4. Increasing Term Insurance

Designed to keep up with inflation.

✔️ Key Features:

- Coverage increases over time

- Premiums may rise

- Protects against cost-of-living increases

👉 Ideal for:

- Long-term protection

- Families concerned about inflation

💰 How Much Life Insurance Do You Need?

Choosing the right coverage amount is crucial. A general rule is to cover:

- 10–15 times your annual income

- Outstanding debts (mortgage, loans)

- Future expenses (education, childcare)

- Daily living costs

Example:

If you earn £30,000 annually, you might consider coverage of £300,000–£450,000.

📊 Factors That Affect Life Insurance Premiums

Life insurance costs vary based on several factors:

🔹 Age

Younger applicants pay lower premiums.

🔹 Health

Medical conditions can increase costs.

🔹 Lifestyle

Smoking, alcohol use, and risky hobbies affect pricing.

🔹 Occupation

High-risk jobs may lead to higher premiums.

🔹 Coverage Amount

Higher coverage means higher premiums.

🔍 How to Compare Life Insurance in the UK

Comparing policies ensures you get the best value.

✔️ Use Comparison Websites

Quickly view multiple quotes and features.

✔️ Check Insurer Reputation

Look at customer reviews and claim settlement rates.

✔️ Understand Policy Terms

Read the fine print, including exclusions and conditions.

✔️ Consider Flexibility

Choose policies that allow adjustments as your needs change.

💡 Tips to Get the Best Life Insurance Deal

✔️ Start Early

The younger you are, the cheaper your premiums.

✔️ Be Honest

Accurate information prevents claim issues later.

✔️ Bundle Policies

Some insurers offer discounts for multiple policies.

✔️ Review Regularly

Update your policy after major life events.

🏠 Life Insurance and Mortgages

Many UK homeowners use life insurance to protect their mortgage.

Why it matters:

- Prevents your family from losing their home

- Ensures debts are cleared

- Provides financial stability

Decreasing term insurance is especially popular for this purpose.

👨👩👧👦 Life Insurance for Families

If you have dependents, life insurance becomes essential.

It helps:

- Replace lost income

- Cover childcare and education costs

- Maintain lifestyle

Stay-at-home parents should also consider coverage, as their contribution has financial value.

💼 Life Insurance for Self-Employed Individuals

Without employer benefits, self-employed individuals need personal protection.

Life insurance can:

- Cover business debts

- Protect business partners

- Ensure family financial security

📈 Benefits of Life Insurance

✔️ Financial Protection

Supports your family when they need it most.

✔️ Peace of Mind

Reduces stress about the future.

✔️ Flexibility

Policies can be tailored to your needs.

✔️ Tax Benefits

In many cases, payouts are tax-free.

⚠️ Common Mistakes to Avoid

❌ Waiting Too Long

Delaying can increase premiums.

❌ Underestimating Coverage

Too little coverage may not meet your family’s needs.

❌ Ignoring Policy Details

Always read terms carefully.

❌ Not Reviewing Your Policy

Life changes—your insurance should too.

🔄 Can You Change Your Life Insurance Policy?

Yes, many policies allow adjustments.

You can:

- Increase or decrease coverage

- Add riders (extra benefits)

- Switch providers

Always check for fees or conditions before making changes.

🌍 The Future of Life Insurance in the UK

The industry is evolving with technology:

📱 Digital Applications

Faster approvals and online management.

🤖 AI Underwriting

More accurate risk assessments.

🧠 Personalised Policies

Tailored coverage based on lifestyle and data.

🧾 Life Insurance vs Critical Illness Cover

These are often confused but serve different purposes.

Life Insurance:

- Pays out on death

Critical Illness Cover:

- Pays out if diagnosed with serious illness

Many people combine both for comprehensive protection.

🏁 Final Thoughts

Life insurance in the UK is not just about money—it’s about responsibility, care, and planning for the future. It ensures that your loved ones are protected, your debts are covered, and your legacy continues.

By understanding your options, comparing policies, and choosing wisely, you can secure a policy that fits your life perfectly.

Remember: the best time to get life insurance is now—before life changes unexpectedly.