💳 Credit Cards for Bad Credit in the USA: Your Complete Guide to Rebuild, Recharge & Rise

In a world where digital wallets, rewards, travel points, and credit scores rule our financial lives, having the right credit card can make all the difference. But what happens when your credit score isn’t high enough to qualify for traditional cards?

Maybe you made mistakes in the past — missed payments, a default, a bankruptcy, or simply little credit history. Whatever the reason, bad credit doesn’t mean financial foreclosure. In fact, it’s the first step in a comeback story that millions in the USA are already writing.

This blog will guide you through everything you need to know about credit cards for bad credit — how they work, the best options available, tips to rebuild your credit, and how to use them smartly to create a strong financial future.

📌 What Does “Bad Credit” Really Mean?

Before diving into cards, let’s understand what bad credit is.

In the USA, your credit score — most commonly a FICO score — ranges from 300 to 850.

Here’s the usual breakdown:

- Excellent: 800–850

- Very Good: 740–799

- Good: 670–739

- Fair: 580–669

- Poor (Bad Credit): Below 580

If your score falls into the poor category, it might be hard to get approved for most mainstream credit cards. But it doesn’t mean you’re blocked from opportunities — you just need the right tools.

🔍 Why Your Credit Score Matters

Your credit score is more than a number — it’s a reputation, a reflection of how responsibly you handle money.

A good score can help you:

✅ Qualify for loans and credit cards with low interest

✅ Get approved for apartments and auto financing

✅ Enjoy lower insurance premiums

✅ Save money in interest payments over time

A bad credit score, on the other hand, often leads to:

❌ Higher APRs (Annual Percentage Rates)

❌ Security deposits on utilities

❌ Limited borrowing options

❌ Higher fees

But here’s the good news:

Bad credit isn’t permanent — and it can be rebuilt systematically.

🧠 How Credit Cards for Bad Credit Work

Credit cards designed for bad credit fall into a few major categories:

1. Secured Credit Cards

These require a security deposit — typically between $200–$500 — which becomes your credit limit.

✔ Easier approval

✔ Helps build positive payment history

✔ Reports to major credit bureaus (Equifax, TransUnion, Experian)

💡 Think of it as a loan you give to yourself — once you build enough credit, you might graduate to a regular card and get your deposit back.

2. Unsecured Credit Cards for Bad Credit

These don’t require a deposit, but often come with:

❌ Higher interest rates

❌ Annual fees

❌ Lower limits

Still, they can be a solid option if you want to start building credit without upfront cash.

3. Cards by Credit Unions or Local Banks

Community banks and credit unions sometimes offer more flexible approval standards compared to big national banks.

🏦 If you’re a member of a credit union, you may find better terms and personal support.

4. Store Credit Cards

Retail store cards (e.g., for department stores or gas stations) are often easier to get approved with bad credit but may carry high interest.

💡 These are best if you want specific store benefits and can pay your balance in full.

📈 Why Using a Credit Card Can Build Your Score

Two major factors affect your credit score:

✔️ Payment History (35%)

Making on‑time payments is the #1 driver of a growing credit score.

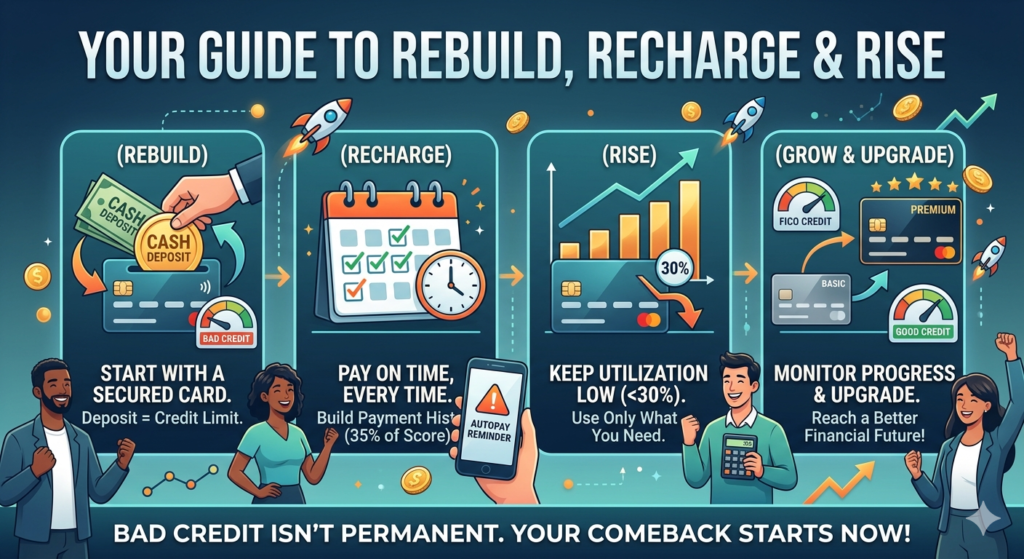

✔️ Credit Utilization (30%)

This is how much of your available credit you use. Ideally:

🔹 Use < 30% of your limit

🔹 Keep your balance low

🔹 Pay before the statement closes

For example: If your limit is $300, keep your balance under $90 — and pay it off each month.

📋 Checklist: What to Look for in a Bad Credit Card

When choosing your card, compare:

🔵 Interest & APR

Lower is better, but high APR is common on bad‑credit cards.

🔵 Annual Fee

Some cards waive it for the first year or forever.

🔵 Reporting to Credit Bureaus

Make sure the card reports to all three major bureaus — this helps rebuild your score faster.

🔵 Upgrade Path

See if the issuer offers a chance to graduate to a better card.

🔵 Fees (Late, Foreign, Cash Advance)

Know what you’re paying before you sign up.

🔥 Common Myths About Bad Credit Cards

❌ Myth: “You’ll never qualify for a credit card”

False — many cards are designed specifically for bad credit.

❌ Myth: “Secured cards don’t help your credit”

Wrong — they absolutely build payment history.

❌ Myth: “You should avoid credit cards if you have bad credit”

Credit, when used responsibly, is one of the fastest ways to improve your score.

💳 Top Features to Prioritize

👉 Automatic credit reporting

👉 No or low annual fee

👉 Reasonable security deposit

👉 Online account access

👉 Mobile alerts and autopay

These features can make your journey easier and more productive.

📌 Step‑by‑Step: How to Rebuild with a Credit Card

Here’s a simple plan that works:

Step 1: Choose the Right Card

Whether secured or unsecured, pick the one with the best terms you can qualify for.

Step 2: Set Up Autopay

Pay your full balance automatically each month.

This helps you avoid late payments — the biggest score killer.

Step 3: Make Small, Regular Purchases

Use the card for essentials you already buy — like groceries or gas — but keep the balance low.

Step 4: Pay Early, Not Later

Even paying before the statement closing date can lower your utilization.

Step 5: Track Your Credit

Check your progress monthly via free tools like Credit Karma, Experian, or AnnualCreditReport.com.

Step 6: Upgrade When Eligible

After 6–12 months of on‑time payments, many issuers will let you graduate to a better card.

📊 Expected Timeline to Improve Your Score

There’s no overnight fix, but with consistent effort:

📅 3 months: On‑time payments start showing positive effects

📅 6–9 months: Noticeable improvement in your score

📅 12+ months: Eligible for better cards and loans

Consistency is the secret ingredient.

📌 Common Mistakes to Avoid

❌ Carrying a high balance

❌ Missing payments

❌ Only paying the minimum

❌ Opening too many cards at once

❌ Ignoring your credit report

Avoid these and you’ll be miles ahead.

💡 Bonus: Using Your Card the Smart Way

Here are strategies the pros use:

✅ Pay Twice a Month

Split payments to lower utilization.

✅ Use Alerts

Enable balance and due‑date alerts in your card app.

✅ Rebuild, Then Relax

Once your score improves, apply for cards with rewards and travel perks.

✅ Don’t Apply for Everything

Hard inquiries can lower your score temporarily. Be selective.

📣 Real People, Real Results

Many Americans started with secured cards and now have strong credit scores. Here’s a typical success story:

“I started with a $300 secured card after a rough year financially. Within 9 months of paying on time, my score jumped 90 points. Now I qualify for rewards cards with travel perks!”

Your turnaround story could be next.

📌 Final Thoughts: Credit Cards Are Tools — Not Temptations

A credit card isn’t a license to spend recklessly. It’s a financial tool — and like any tool, its impact depends on how responsibly you use it.

Used smartly:

✔ It builds credit

✔ Opens financial doors

✔ Improves your borrowing power

✔ Reduces stress over time

Used carelessly:

❌ It can trap you in debt

❌ Hurt your credit

❌ Cost you money in interest

Let’s Recap

A good path forward includes:

📌 Knowing your credit score

📌 Choosing the right card

📌 Paying on time 100% of the time

📌 Keeping balances low

📌 Monitoring progress

Bad credit isn’t a setback — it’s a beginning. With the right mindset and tools, you can turn your credit story around faster than you think.

Are You Ready to Rebuild Your Credit?

Your financial recovery journey starts with one step — pick the card that fits your needs, use it wisely, and let time work in your favor.

Remember: Your past doesn’t define your future — your habits do.