Business Loans in the UK

Starting, running, or expanding a business often requires capital. In the UK, business loans are one of the most accessible and flexible ways to fund your venture, whether you’re a startup, an SME, or an established enterprise. Understanding how business loans work, the types available, and how to choose the right one is essential for long-term financial success.

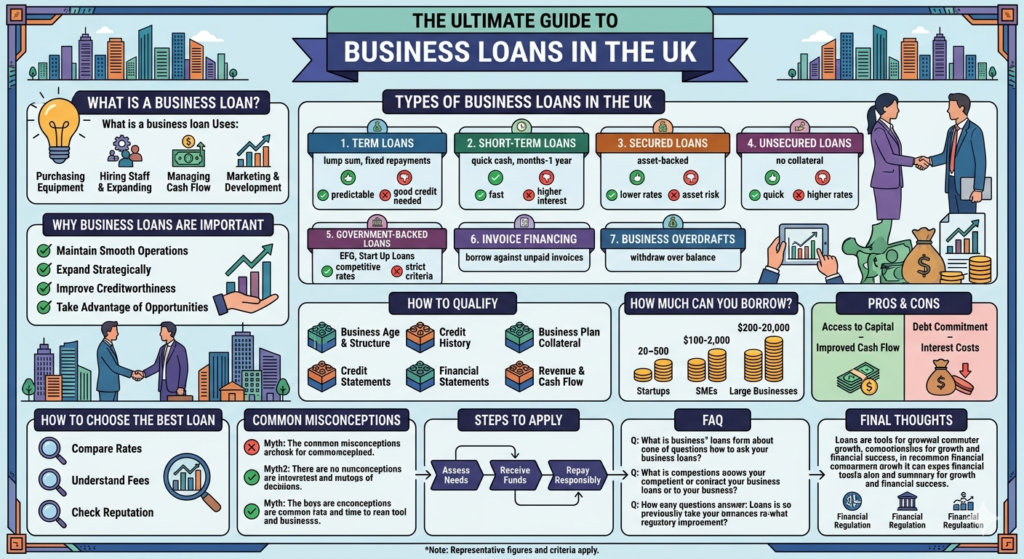

What is a Business Loan?

A business loan is a financial product designed to provide funds to businesses for operational or growth purposes. Unlike personal loans, business loans are specifically structured to support business activities, such as:

- Purchasing equipment or inventory

- Hiring staff or expanding operations

- Managing cash flow and day-to-day expenses

- Marketing and business development

- Refinancing existing business debts

Business loans in the UK come from a variety of sources, including banks, online lenders, government-backed schemes, and peer-to-peer lending platforms.

Why Business Loans are Important

Access to capital is crucial for any business. Even profitable companies may face cash flow challenges, seasonal demands, or opportunities for expansion that require immediate funds. Business loans help businesses:

- Maintain Smooth Operations – Covering short-term expenses like payroll, utilities, or inventory.

- Expand Strategically – Financing new locations, product lines, or technologies.

- Improve Creditworthiness – Timely repayment can boost your business credit score, making future funding easier.

- Take Advantage of Opportunities – Quick access to funds allows businesses to seize growth opportunities or respond to market changes.

Types of Business Loans in the UK

UK lenders offer various business loan options tailored to different needs, risk profiles, and repayment capacities.

1. Term Loans

Term loans are the most common type of business loan. They provide a lump sum upfront, which is repaid in regular installments over a fixed period, typically 1–10 years.

Pros:

- Fixed interest rates make budgeting easier

- Predictable repayment schedule

- Suitable for long-term investments

Cons:

- Requires good credit and business history

- May involve collateral

2. Short-Term Loans

Short-term business loans provide smaller amounts over a period of a few months to a year. They are ideal for:

- Covering cash flow gaps

- Meeting urgent operational expenses

- Managing seasonal demand

Pros:

- Quick approval

- Flexible repayment terms

Cons:

- Higher interest rates than long-term loans

- Not suitable for large capital investments

3. Secured Loans

Secured business loans are backed by an asset, such as property, equipment, or inventory. Collateral reduces the lender’s risk, often resulting in lower interest rates and higher borrowing limits.

Pros:

- Larger loan amounts

- Lower interest rates

Cons:

- Risk of losing the asset if repayments are missed

- Longer approval process due to asset valuation

4. Unsecured Loans

Unsecured loans don’t require collateral. These are usually suitable for small to medium-sized loans for startups or businesses without substantial assets.

Pros:

- No collateral required

- Quick approval for eligible businesses

Cons:

- Higher interest rates

- Lower borrowing limits

5. Government-Backed Loans

The UK government provides schemes to support businesses, especially startups or SMEs. Popular options include:

- Enterprise Finance Guarantee (EFG): Supports businesses with limited collateral by guaranteeing a portion of the loan.

- Start Up Loans Scheme: Provides affordable loans and mentoring for new businesses.

- British Business Bank Programs: Offers funding through participating lenders to support growth-oriented SMEs.

Pros:

- Lower risk for lenders

- Competitive interest rates

- Additional business support and mentoring

Cons:

- Eligibility criteria may be strict

- Application process can be more complex

6. Invoice Financing

Invoice financing allows businesses to borrow against unpaid invoices. This is a short-term solution to improve cash flow.

Pros:

- Fast access to cash

- Helps manage cash flow

Cons:

- Fees may be high

- Only suitable for businesses with outstanding invoices

7. Business Overdrafts

A business overdraft allows you to withdraw more money than is in your business account, up to an agreed limit. Interest is charged only on the amount overdrawn.

Pros:

- Flexible access to funds

- Ideal for short-term cash flow issues

Cons:

- High interest rates if used extensively

- Not suitable for long-term investments

How to Qualify for a Business Loan in the UK

Eligibility depends on the lender, loan type, and your business profile. Common factors include:

- Business Age and Structure – Many lenders require at least 1–2 years of trading for established businesses.

- Credit History – Both personal and business credit scores are considered. A strong credit history improves chances of approval.

- Financial Statements – Profit and loss statements, balance sheets, and cash flow projections are often required.

- Business Plan – For startups, a clear and viable business plan is critical.

- Collateral – Required for secured loans; the value of the asset influences loan size.

- Revenue and Cash Flow – Demonstrates your ability to repay the loan on time.

How Much Can You Borrow?

The borrowing limit depends on factors like business revenue, cash flow, loan type, and collateral. In the UK:

- Startups: £1,000–£25,000 (via government schemes or online lenders)

- SMEs: £25,000–£500,000+ depending on profitability and security

- Large Businesses: £500,000+ with secured lending or specialized financing

Pros and Cons of Business Loans

Advantages

- Access to Capital – Enables growth, expansion, and operational stability.

- Improved Cash Flow – Smooths over financial fluctuations, especially for seasonal businesses.

- Flexible Options – Multiple loan types to suit specific business needs.

- Build Credit History – Timely repayments improve both business and personal credit profiles.

- Tax Benefits – Interest on business loans can often be tax-deductible.

Disadvantages

- Debt Commitment – Regular repayments are mandatory regardless of business performance.

- Risk to Assets – Secured loans can result in asset loss if repayment fails.

- Interest Costs – Long-term borrowing increases total interest paid.

- Eligibility Barriers – Startups or businesses with poor credit may face challenges.

How to Choose the Best Business Loan in the UK

Choosing the right loan requires careful assessment of your business’s financial needs, risk tolerance, and repayment ability. Consider these tips:

- Compare Interest Rates – Even a 1% difference can save thousands over the loan term.

- Understand Fees – Check arrangement fees, early repayment charges, and hidden costs.

- Evaluate Repayment Flexibility – Overpayments, payment holidays, or early repayment options can improve financial control.

- Check Lender Reputation – Opt for regulated UK lenders for security and transparency.

- Seek Professional Advice – Accountants, financial advisors, or business mentors can provide tailored recommendations.

Common Misconceptions About Business Loans

Misconception 1: Only Big Companies Get Loans

Many startups and SMEs successfully secure loans in the UK. Government-backed schemes and online lenders have made borrowing accessible to small businesses.

Misconception 2: Loans Are Expensive

With the right loan type, interest rates can be competitive, especially for secured loans or government-backed schemes.

Misconception 3: Personal Guarantees Are Always Required

Not all business loans require a personal guarantee. However, for startups or riskier applications, lenders may request it to reduce risk.

Steps to Apply for a Business Loan in the UK

- Assess Your Needs – Determine the amount, purpose, and repayment capability.

- Research Lenders – Compare banks, online lenders, and government schemes.

- Prepare Documentation – Gather financial statements, business plan, credit reports, and identification.

- Submit Application – Provide all required information accurately.

- Negotiate Terms – Ensure interest rates, repayment schedules, and fees are clear.

- Receive Funds – Once approved, the loan amount is disbursed to your business account.

- Repay Responsibly – Timely repayments maintain a healthy credit profile and reduce costs.

Frequently Asked Questions

Q1: Can startups get business loans in the UK?

Yes, through schemes like Start Up Loans, government-backed guarantees, or online lenders, even new businesses can access funding.

Q2: Are business loans tax-deductible?

Interest on loans used for business purposes is typically tax-deductible, reducing overall costs.

Q3: How long does it take to get a business loan?

Approval time varies: online lenders can provide funds in a few days, while banks and government schemes may take weeks.

Q4: What happens if I miss payments?

Missed payments can affect your credit rating and may lead to penalties. For secured loans, collateral could be repossessed.

Final Thoughts

Business loans in the UK are essential tools for growth, stability, and strategic development. They offer flexibility, access to larger capital, and opportunities for businesses of all sizes. By understanding loan types, eligibility requirements, and repayment options, business owners can make informed decisions that propel their company forward.

Whether you’re launching a startup, expanding operations, or managing cash flow, the right business loan can be the difference between stagnation and success. With careful planning, responsible borrowing, and strategic use of funds, business loans become a powerful ally for financial growth.