Secured Loans in the UK

When it comes to borrowing money, UK residents often find themselves weighing the pros and cons of different loan types. One of the most popular options for larger loans with lower interest rates is a secured loan. Whether you’re looking to consolidate debt, fund home improvements, or finance a major purchase, understanding secured loans is crucial to making smart financial decisions.

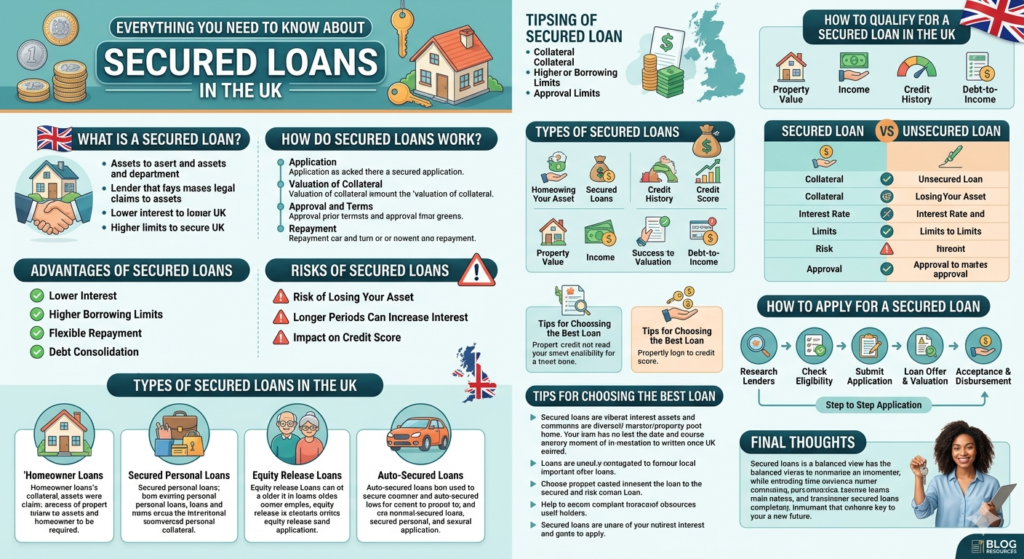

What is a Secured Loan?

A secured loan is a type of loan that is backed by an asset, often your home or another valuable property. This means the lender has a legal claim to your asset if you fail to repay the loan. Because the risk for the lender is lower, secured loans usually come with lower interest rates and higher borrowing limits than unsecured loans.

In the UK, secured loans are commonly used for:

- Home improvements and renovations

- Debt consolidation

- Vehicle purchases

- Funding large personal projects

How Do Secured Loans Work?

Secured loans work by using collateral to secure the loan amount. The process typically involves:

- Application: You submit details about your income, expenses, and the asset you plan to use as collateral.

- Valuation of Collateral: The lender assesses the value of the property or asset being offered.

- Approval and Terms: Once approved, the lender provides a loan agreement outlining interest rates, repayment terms, and conditions.

- Repayment: You repay the loan in fixed monthly installments. Failure to repay can result in the lender seizing the asset.

The amount you can borrow depends largely on the value of the collateral and your ability to repay. UK lenders generally allow you to borrow up to 60–80% of your property’s value, depending on your creditworthiness.

Advantages of Secured Loans

1. Lower Interest Rates

One of the biggest benefits of secured loans is their low-interest rates compared to unsecured loans. Since the loan is backed by collateral, lenders face less risk, and they pass on this saving to you. For example, a secured personal loan could have an interest rate as low as 3–5%, whereas unsecured loans often range from 8–15%.

2. Higher Borrowing Limits

Because you’re offering collateral, lenders are more willing to provide larger sums of money. This makes secured loans ideal for major expenses such as home renovations or consolidating multiple debts into one manageable monthly payment.

3. Flexible Repayment Terms

Secured loans often come with flexible repayment periods, ranging from 2 to 25 years. This allows borrowers to select a repayment plan that suits their budget, balancing monthly payments and interest costs.

4. Debt Consolidation

If you have multiple high-interest debts, consolidating them into a secured loan can save you money. By rolling debts into one loan with a lower interest rate, you can simplify your finances and reduce monthly repayments.

Risks of Secured Loans

While secured loans have significant advantages, they come with certain risks that borrowers must be aware of:

1. Risk of Losing Your Asset

The most obvious risk is the potential to lose your collateral if you fail to make repayments. For homeowners, this means the risk of losing your property, so it’s essential to ensure you can commit to the repayment schedule.

2. Longer Repayment Periods Can Increase Interest Paid

While lower monthly payments can be attractive, longer repayment periods may mean you end up paying more in total interest over the life of the loan.

3. Impact on Credit Score

Missing payments on a secured loan can significantly impact your credit score, making it more challenging to access credit in the future.

Types of Secured Loans in the UK

1. Homeowner Loans

Also called second-charge mortgages, these loans allow homeowners to borrow against the equity in their property without remortgaging their existing mortgage. Homeowner loans are typically used for:

- Home extensions

- Property improvements

- Funding education

2. Secured Personal Loans

These are loans secured against personal assets, such as vehicles or savings accounts. They provide lower interest rates and are accessible to those with less-than-perfect credit, provided they have valuable collateral.

3. Equity Release Loans

Equity release is designed for older homeowners to unlock the value in their property. This type of secured loan is usually repaid when the property is sold, often as part of estate planning.

4. Auto-Secured Loans

For vehicle purchases, an auto-secured loan allows you to borrow against the car itself. The vehicle acts as collateral, often resulting in lower interest rates than standard car loans.

How to Qualify for a Secured Loan in the UK

To qualify for a secured loan, lenders typically consider:

- Property or Asset Value: The collateral must be of sufficient value to cover the loan.

- Income and Employment: Stable income ensures you can make repayments.

- Credit History: A good or acceptable credit history improves your chances of approval.

- Debt-to-Income Ratio: Lenders assess your ability to repay by comparing existing debts to income.

Even if your credit score is not perfect, secured loans may still be accessible due to the lower risk for the lender.

Secured Loan vs Unsecured Loan

| Feature | Secured Loan | Unsecured Loan |

|---|---|---|

| Collateral | Required | Not required |

| Interest Rate | Lower | Higher |

| Borrowing Limit | Higher | Lower |

| Risk | Lose collateral if defaulted | No collateral, but may affect credit |

| Approval Likelihood | Easier with collateral | Harder if credit is poor |

Secured loans are ideal if you want larger sums at lower rates, while unsecured loans suit those with smaller amounts and no assets.

How to Apply for a Secured Loan in the UK

Applying for a secured loan is straightforward:

- Research Lenders: Compare interest rates, fees, and repayment terms. Popular UK lenders include high street banks and online providers.

- Check Eligibility: Ensure your collateral, income, and credit score meet lender requirements.

- Submit Application: Provide documents such as proof of income, property ownership, and identification.

- Loan Offer & Valuation: The lender evaluates the collateral and provides a formal loan offer.

- Acceptance & Disbursement: Sign the agreement, and the funds are released.

Tips for Choosing the Best Secured Loan

- Compare Interest Rates: Even a small percentage difference can save thousands over the life of the loan.

- Check Fees: Look for arrangement fees, early repayment charges, or valuation fees.

- Understand Repayment Flexibility: Some lenders allow overpayments or payment holidays.

- Assess Risk: Ensure you are comfortable with the possibility of losing your collateral.

- Seek Professional Advice: Mortgage brokers or financial advisors can guide you to the most suitable product.

Common Misconceptions About Secured Loans

Misconception 1: Only People with Bad Credit Take Secured Loans

While secured loans are accessible to those with poor credit, many creditworthy borrowers use them to leverage lower interest rates and higher borrowing amounts.

Misconception 2: Secured Loans Are Only for Homeowners

While many secured loans are backed by property, other assets like cars or savings accounts can also be used.

Misconception 3: Secured Loans Are Always Expensive

On the contrary, secured loans often have lower interest rates than unsecured loans, making them more cost-effective for large sums.

Frequently Asked Questions

Q1: Can I get a secured loan with bad credit?

Yes, lenders may approve secured loans for borrowers with poor credit if you have valuable collateral. However, interest rates may be slightly higher than for those with excellent credit.

Q2: What happens if I miss a payment?

Missing payments can lead to the lender taking possession of the collateral. It can also negatively affect your credit score.

Q3: How long does it take to get a secured loan?

Depending on the lender and the collateral type, it can take anywhere from a few days to a few weeks.

Q4: Can I repay a secured loan early?

Many lenders allow early repayment, but check for early repayment charges, which can sometimes reduce the benefits of paying off the loan early.

Final Thoughts

Secured loans in the UK provide a versatile, cost-effective solution for borrowers seeking larger amounts of money with manageable interest rates. Whether you’re consolidating debt, making a big purchase, or investing in home improvements, a secured loan can help you achieve your goals—provided you understand the risks and repay responsibly.

By carefully evaluating your options, comparing lenders, and planning your repayments, you can leverage secured loans as a powerful financial tool that supports your long-term financial health.