Imagine getting rewarded every time you spend money—on groceries, fuel, online shopping, or even your monthly bills. Sounds like a win-win, right? That’s exactly what cashback credit cards in the UK offer: the chance to turn everyday spending into real financial rewards.

Whether you’re a savvy shopper or someone looking to make smarter financial choices, cashback credit cards can help you stretch your money further—without changing your lifestyle.

Let’s dive deep into this exciting world and uncover how you can make the most of it.

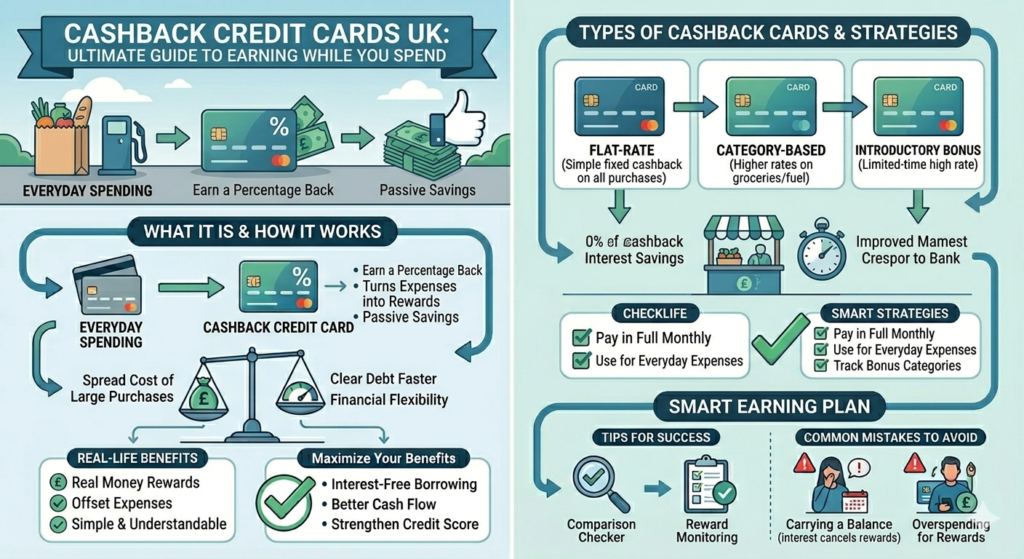

What Is a Cashback Credit Card?

A cashback credit card gives you a percentage of your spending back as cash rewards.

For example:

- Spend £100

- Earn 1% cashback

- Get £1 back

It may seem small at first, but over time, these rewards can add up significantly—especially if you use your card for regular expenses.

How Do Cashback Credit Cards Work?

The concept is simple:

- You use your credit card for purchases

- The card provider tracks your spending

- A percentage is returned to you as cashback

This cashback is usually:

- Credited to your account

- Paid annually

- Redeemed as statement credit or bank transfer

Types of Cashback Credit Cards in the UK

Different cards suit different spending habits. Let’s explore the main types.

1. Flat-Rate Cashback Cards

These offer a fixed cashback rate on all purchases.

- Example: 1% on everything

- Simple and predictable

Best for: People who want straightforward rewards.

2. Tiered Cashback Cards

Cashback increases based on spending levels.

- 0.5% on first £5,000

- 1% after that

Best for: High spenders.

3. Category-Based Cashback Cards

Higher cashback in specific categories like:

- Supermarkets

- Fuel

- Travel

Best for: Targeted spending.

4. Introductory Bonus Cards

Offer higher cashback for a limited time.

- Example: 5% cashback for first 3 months

Best for: Maximizing short-term rewards.

Key Features to Look For

✔ Cashback Rate

The percentage you earn on spending.

✔ Annual Fee

Some cards charge fees—but may offer higher rewards.

✔ Payment Frequency

Monthly, yearly, or upon reaching a threshold.

✔ Spending Caps

Limits on how much cashback you can earn.

Why Cashback Credit Cards Are So Popular

💷 Earn While You Spend

Turn everyday purchases into savings.

🧾 Passive Rewards

No extra effort required.

📉 Offset Expenses

Use cashback to reduce your bills.

🎯 Financial Motivation

Encourages smarter spending habits.

Real-Life Example

Let’s say you spend:

- £800 per month on your card

- Cashback rate: 1%

Monthly cashback: £8

Yearly cashback: £96

That’s nearly £100 back—just for spending as usual.

Who Should Use Cashback Credit Cards?

These cards are ideal for:

- Regular credit card users

- People who pay balances in full each month

- Budget-conscious individuals

- Families with consistent expenses

Advantages of Cashback Credit Cards

🔹 Real Money Rewards

Unlike points, cashback is flexible.

🔹 Easy to Understand

No complicated redemption systems.

🔹 Works with Everyday Spending

Groceries, bills, shopping—all count.

🔹 Stack with Other Offers

Combine with discounts and promotions.

Potential Drawbacks

⚠ Interest Charges

If you don’t pay in full, interest can outweigh cashback.

⚠ Spending Temptation

Rewards may encourage unnecessary purchases.

⚠ Caps and Limits

Some cards restrict earnings.

⚠ Annual Fees

Must be justified by rewards.

How to Maximize Your Cashback

✅ Pay in Full Every Month

Avoid interest charges.

✅ Use for Everyday Expenses

Groceries, fuel, subscriptions.

✅ Track Bonus Categories

Maximize higher cashback areas.

✅ Combine with Offers

Use retailer discounts alongside cashback.

Choosing the Best Cashback Credit Card in the UK

🔍 Compare Cashback Rates

Higher isn’t always better—check conditions.

💸 Consider Fees

Ensure rewards outweigh costs.

📊 Understand Your Spending

Pick a card that matches your habits.

📄 Read the Fine Print

Know limits and exclusions.

Cashback vs Reward Points Cards

Cashback Cards:

- Simple

- Flexible

- Direct value

Reward Cards:

- Points or miles

- May offer higher value if used strategically

Choose based on your lifestyle.

Common Mistakes to Avoid

❌ Carrying a Balance

Interest cancels out rewards.

❌ Ignoring Limits

Caps can reduce earnings.

❌ Overspending for Rewards

Spend only what you need.

❌ Missing Payments

Can lead to fees and lost benefits.

How Cashback Cards Affect Your Credit Score

Used responsibly, they can:

- Improve payment history

- Increase credit utilization ratio control

- Build a strong credit profile

But misuse can harm your score.

Psychological Benefits

Cashback cards offer more than money:

- Satisfaction from earning rewards

- Motivation to manage finances

- Sense of control over spending

Long-Term Financial Impact

Over time, cashback cards can:

- Reduce overall expenses

- Improve financial habits

- Increase savings

They reward discipline and consistency.

Are Cashback Cards Worth It?

Absolutely—if used correctly.

They’re best for people who:

- Spend regularly

- Pay balances in full

- Understand how rewards work

When Should You Avoid Them?

Avoid cashback cards if:

- You struggle with debt

- You tend to overspend

- You can’t pay balances monthly

In such cases, simpler financial tools may be better.

Alternatives to Cashback Cards

- 0% interest credit cards

- Balance transfer cards

- Debit card rewards programs

Each serves a different purpose.

Expert Tips

- Set a monthly spending budget

- Use one primary cashback card

- Monitor your rewards regularly

- Upgrade cards as your credit improves

Final Thoughts

Cashback credit cards in the UK are a smart way to make your money work harder. They transform everyday spending into tangible rewards—helping you save without changing your lifestyle.

But remember:

The real benefit comes from discipline, planning, and responsible use.

Your Next Step

Ready to start earning while you spend?

- Compare cashback cards

- Match them to your spending habits

- Use them wisely

And watch your everyday purchases turn into real savings.