In today’s fast-paced financial world, credit cards can be both a blessing and a burden. While they offer convenience and flexibility, high-interest debt can quickly spiral out of control. If you’re struggling with multiple credit card balances, there’s a powerful financial tool that could help you regain control: balance transfer credit cards.

This comprehensive guide will walk you through everything you need to know about balance transfer credit cards in the USA—how they work, their benefits, potential drawbacks, and how to use them wisely to become debt-free faster.

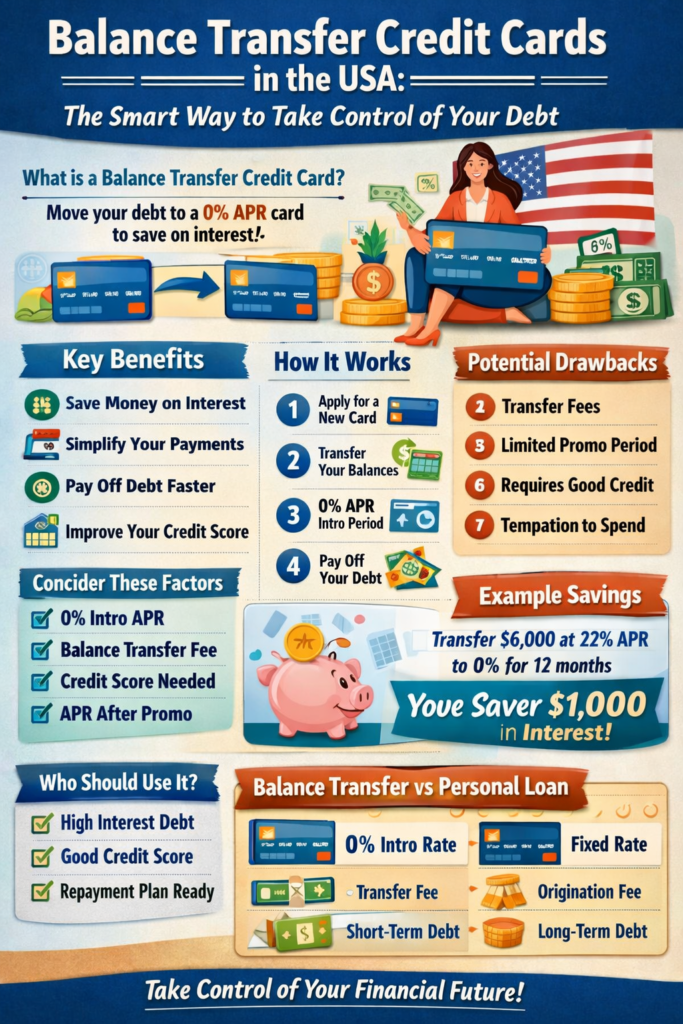

What Is a Balance Transfer Credit Card?

A balance transfer credit card allows you to move existing debt from one or more credit cards onto a new card—typically with a low or 0% introductory APR (Annual Percentage Rate) for a limited period.

This means you can pay off your debt without accumulating high interest, which can save you hundreds or even thousands of dollars.

How Does a Balance Transfer Work?

Here’s a simple breakdown:

- You apply for a balance transfer credit card.

- Once approved, you request to transfer balances from your existing cards.

- The new card issuer pays off your old balances.

- You now owe the balance on the new card—often at 0% interest for a promotional period.

This promotional period usually lasts 6 to 21 months, depending on the card.

Key Benefits of Balance Transfer Credit Cards

1. Save Money on Interest

High-interest credit cards often charge 18%–30% APR. With a 0% balance transfer offer, every payment you make goes directly toward reducing your principal balance.

2. Simplify Your Finances

Instead of juggling multiple payments, you consolidate your debt into one easy monthly payment.

3. Pay Off Debt Faster

Without interest slowing you down, you can eliminate debt much more quickly.

4. Improve Credit Score Over Time

By reducing your credit utilization and making consistent payments, your credit score can gradually improve.

Common Features to Look For

When choosing a balance transfer credit card, consider these features:

0% Introductory APR

The longer the promotional period, the more time you have to pay off your debt interest-free.

Balance Transfer Fee

Most cards charge 3% to 5% of the transferred amount. For example, transferring $5,000 with a 3% fee costs $150.

Regular APR After Promo

Once the intro period ends, the APR can jump significantly. Make sure you know this rate.

Credit Limit

Your approved limit determines how much debt you can transfer.

Top Reasons Americans Use Balance Transfer Cards

- Paying off high-interest credit card debt

- Consolidating multiple credit accounts

- Managing unexpected expenses

- Avoiding personal loans with higher rates

Potential Drawbacks You Should Know

While balance transfer cards are powerful, they’re not perfect.

1. Transfer Fees

Even with 0% interest, fees can add up.

2. Limited Promotional Period

If you don’t pay off the balance in time, interest kicks in.

3. Requires Good Credit

Most top offers require a good to excellent credit score (670+).

4. Temptation to Spend More

Opening a new card may lead to additional spending—defeating the purpose.

Who Should Use a Balance Transfer Credit Card?

This strategy is ideal for people who:

- Have high-interest credit card debt

- Can commit to a repayment plan

- Have a good credit score

- Want to save money on interest

It may not be suitable if:

- You struggle with overspending

- You can’t pay off debt within the promo period

- Your credit score is low

Step-by-Step Guide to Using a Balance Transfer Card

Step 1: Check Your Credit Score

Before applying, review your credit score to ensure you qualify for the best offers.

Step 2: Compare Offers

Look for cards with:

- Long 0% APR periods

- Low transfer fees

- No annual fee

Step 3: Apply for the Card

Fill out an online application. Approval can take minutes to a few days.

Step 4: Transfer Your Balances

Initiate the transfer through your new card issuer.

Step 5: Create a Repayment Plan

Divide your total balance by the number of months in the promo period.

Step 6: Avoid New Purchases

Focus only on paying off your transferred balance.

Example: How Much Can You Save?

Let’s say you have $6,000 in credit card debt at 22% APR.

- Without transfer: You could pay over $1,300 in interest in a year.

- With a 0% balance transfer (12 months): You pay $0 interest, plus maybe a small transfer fee.

That’s a huge saving—and a faster path to becoming debt-free.

Tips to Maximize Your Balance Transfer Strategy

Pay More Than the Minimum

Minimum payments will not eliminate your debt within the promo period.

Set Automatic Payments

Avoid late fees and protect your credit score.

Track Your Progress

Keep an eye on your remaining balance and timeline.

Don’t Miss Payments

Late payments can cancel your 0% APR offer.

Avoid New Debt

Stay disciplined—this is your chance to reset financially.

Balance Transfer vs Personal Loan

| Feature | Balance Transfer Card | Personal Loan |

|---|---|---|

| Interest Rate | 0% (intro period) | Fixed rate |

| Flexibility | High | Moderate |

| Fees | Transfer fee | Origination fee |

| Best For | Short-term debt | Larger, long-term debt |

Both options have their place, but balance transfer cards are often better for short-term debt elimination.

How to Choose the Best Balance Transfer Card

When evaluating options, ask yourself:

- How long is the 0% APR period?

- What is the transfer fee?

- Is there an annual fee?

- What happens after the intro period?

The best card is one that matches your repayment ability and financial goals.

Mistakes to Avoid

- ❌ Ignoring the transfer fee

- ❌ Missing payments

- ❌ Using the card for new purchases

- ❌ Not having a repayment plan

- ❌ Waiting too long to transfer balances

Avoiding these mistakes can make the difference between success and deeper debt.

Are Balance Transfer Credit Cards Worth It?

For many Americans, the answer is yes.

If used correctly, these cards can:

- Save significant money on interest

- Simplify financial management

- Help you get out of debt faster

However, success depends on discipline and planning.

Final Thoughts: Take Control of Your Financial Future

Balance transfer credit cards are more than just a financial product—they’re a strategy for freedom. When used wisely, they can help you break free from the cycle of high-interest debt and build a stronger financial future.

The key is simple:

- Choose the right card

- Stick to a repayment plan

- Stay disciplined

Your journey to financial stability starts with one smart decision—and a balance transfer credit card could be that turning point.