If you’re a homeowner with a mortgage, refinancing might be one of the smartest financial moves you can make — or delay — depending on current interest rates and your goals. Here’s a clear, up-to-date look at mortgage refinance rates in the USA and how to decide if now’s the right time to refinance 👇

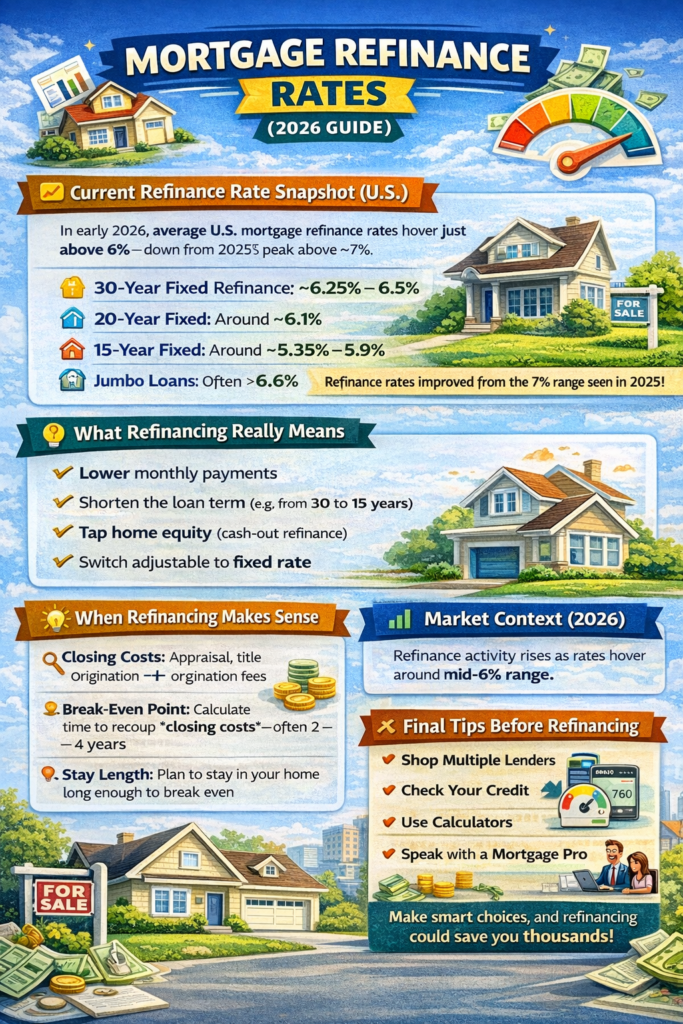

📊 Current Refinance Rate Snapshot (U.S.)

As of early February 2026, mortgage refinance rates in the U.S. have remained just above 6% for many loan types — a level that’s attractive for some homeowners compared with the higher rates seen in recent years: �

Forbes +1

🏠 30-Year Fixed Refinance: ~6.25% – 6.56% average, depending on lender surveys. �

Forbes +1

📉 20-Year Fixed Refinance: Around ~6.1% – 6.14%. �

Forbes

🏃♂️ 15-Year Fixed Refinance: Around ~5.35% – 5.9%, typically the lowest among standard options. �

Forbes +1

💼 Jumbo Loans: Higher, often above ~6.6% for large-loan refis. �

Forbes

Mortgage rates have trended lower compared with early 2025 peaks (above ~7%) but are still well above the historic pandemic lows near 2–3%. �

AInvest

📈 Why this matters: Lower refinance rates mean you could reduce your monthly payment, shorten your loan term, or save thousands in long-term interest — but only if the new rate is meaningfully lower than your current one.

📌 What Refinancing Really Means

Refinancing replaces your current mortgage with a new one — ideally at a lower interest rate or better terms. Homeowners usually refinance to:

✔ Lower monthly payments

✔ Shorten the loan term (e.g., from 30 to 15 years)

✔ Tap home equity for cash (cash-out refinance)

✔ Switch from an adjustable-rate to a fixed-rate mortgage

🧠 When Refinancing Makes Sense

Here are some rules of thumb that financial experts often use:

🔹 Interest Rate Drop: If you can reduce your rate by at least ~0.75 – 1% compared to your current mortgage, refinancing could pay off over time. �

🔹 Break-Even Point: Calculate how long it will take to recoup closing costs — often 2 – 4 years or more before savings exceed the refinance expense. �

🔹 Stay Length: If you plan to stay in your home long enough to benefit from lower payments, refinancing becomes more valuable.

Federal Reserve

Federal Reserve

💡 For example: If you have a current rate of ~7% and can refinance into ~6.25%, monthly savings and long-term interest reduction could add up. But if your current rate is already similar to today’s, the benefit may be minimal.

🧩 Things to Watch Out For

🔎 Closing Costs: Refinancing typically involves costs — appraisal, title fees, origination fees — which must be weighed against your monthly savings. �

🔎 Loan Term Reset: Extending a new 30-year term might lower payments today but could increase total interest over the life of the loan. �

🔎 Equity Requirements: Most lenders want at least ~20% home equity for the best refinance rates.

Federal Reserve

Federal Reserve

📉 Market Context (2026)

Mortgage refinance activity has grown as rates hovered around their lowest levels in several years — near the mid-6% range for 30-year refinances — although many homeowners remain “locked in” to older, lower rates and aren’t refinancing immediately. �

Bankrate

📊 Analysts expect rates to stay above ~6% for much of the year, though small dips are possible depending on Federal Reserve actions and economic trends.

🔍 Final Tips Before You Refinance

✨ Shop Multiple Lenders: Rates and fees vary widely; get quotes from several lenders.

✨ Check Your Credit: A higher score can unlock better rates.

✨ Use Calculators: Online refinance calculators can estimate monthly savings and break-even time.

✨ Speak with a Mortgage Pro: Personalized guidance helps you avoid costly mistakes.