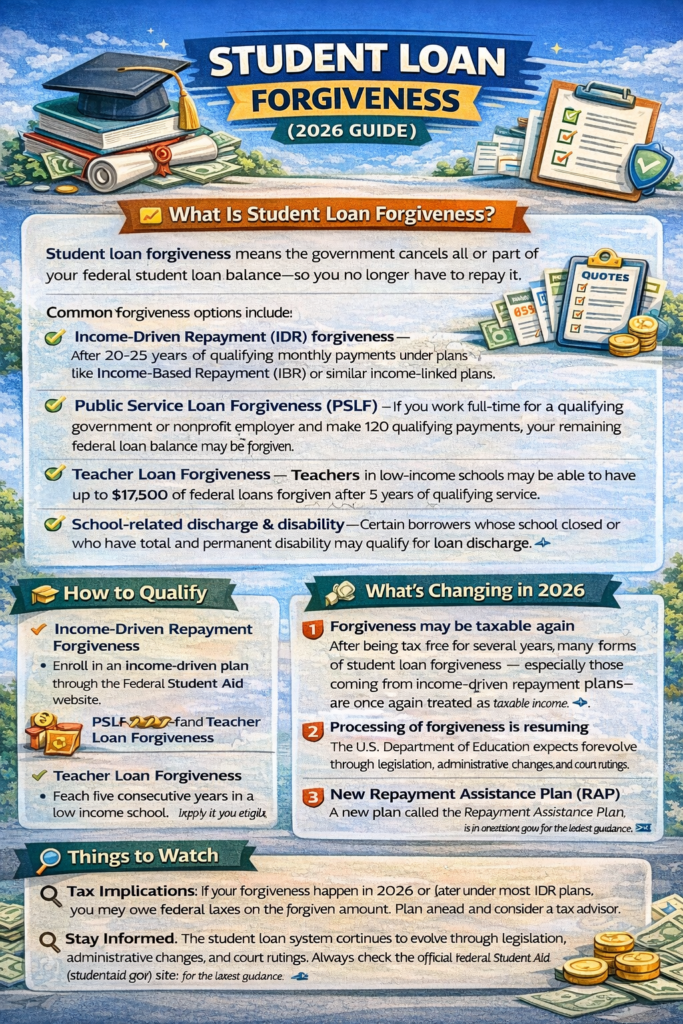

👇—🎓 Student Loan Forgiveness — What Borrowers Need to Know (2026 Guide)Student loan forgiveness can be a lifeline for borrowers, wiping out all or part of your federal student loan debt after meeting certain requirements. It’s designed to ease the financial burden of education costs — but the rules and tax treatment have shifted recently. Here’s a simple guide to what it is, how it works, and what’s new in 2026.—📌 What Is Student Loan Forgiveness?Student loan forgiveness means the government cancels all or part of your federal student loan balance — so you no longer have to repay it. Common forgiveness options include:✅ Income‑Driven Repayment (IDR) forgiveness — After 20‑25 years of qualifying monthly payments under plans like Income‑Based Repayment (IBR) or similar income‑linked plans, any remaining balance may be forgiven. ✅ Public Service Loan Forgiveness (PSLF) — If you work full‑time for a qualifying government or nonprofit employer and make 120 qualifying payments, your remaining federal loan balance may be forgiven. ✅ Teacher Loan Forgiveness — Teachers in low‑income schools may be able to have up to $17,500 of federal loans forgiven after five years of qualifying service. ✅ School‑related discharge & disability — Certain borrowers whose school closed or who have total and permanent disability may qualify for loan discharge. These programs apply only to federal student loans; private student loans usually do not qualify. —📊 What’s Changing in 20261. Forgiveness may be taxable againAfter being tax‑free for several years, many forms of student loan forgiveness — especially those coming from income‑driven repayment plans — are once again treated as taxable income at the federal level starting in 2026. That means the forgiven amount may be counted as income on your tax return and could increase your tax bill. Certain forgiveness programs — like PSLF and Teacher Loan Forgiveness — remain tax‑free. 2. Processing of forgiveness is resumingForgiveness processing under plans such as the Income‑Based Repayment plan has been paused at various times due to administrative updates and court actions, but the U.S. Department of Education has stepped in to resume processing for eligible borrowers and expects these discharges to continue. 3. New Repayment Assistance Plan (RAP)A new plan called the Repayment Assistance Plan (RAP) is expected to take effect by mid‑2026. RAP aims to provide affordable, income‑linked payments over a longer term (up to 30 years) before forgiveness, similar in purpose to the popular SAVE plan. —🧠 How to QualifyIncome‑Driven Repayment ForgivenessEnroll in an income‑driven plan through the Federal Student Aid website.Make required payments for 20–25 years (based on your plan), calculated using your income and family size.Any remaining balance at the end of the term may be forgiven. Public Service Loan Forgiveness (PSLF)Work full‑time for a qualifying employer (government or nonprofit).Make 120 qualifying payments under a qualifying plan.Submit annual employer certification and stay on track with the PSLF Help Tool. Teacher Loan ForgivenessTeach five consecutive years in a low‑income school.Apply through your loan servicer once eligible. Other DischargesClosed school and disability discharges require specific documentation and eligibility criteria. —📌 Things to Watch🔎 Tax Implications: If your forgiveness happens in 2026 or later under most IDR plans, you may owe federal taxes on the forgiven amount. Plan ahead and consider consulting a tax advisor. 🔎 Stay Informed: The student loan system continues to evolve through legislation, administrative changes, and court rulings. Always check the official Federal Student Aid (studentaid.gov) site for the latest guidance. 🔎 Beware of Scams: You never have to pay to apply for forgiveness — official applications are free through federal channels. —💡 Final ThoughtStudent loan forgiveness can be a powerful tool to reduce debt and improve financial freedom — but understanding the eligibility rules, payment requirements, and potential tax impact in 2026 is essential. Stay informed, track your qualifying payments, and talk to your loan servicer or financial advisor to make the most of available options.